Discrete Markov Chains

Overview

Teaching: min

Exercises: minQuestions

Objectives

Infinite Discrete Markov Chains

All of the Markov chains we have until now have had a finite number of states. In this chapter, we consider Markov chains with a countably infinite number of states. That is, they are still discrete, but can take on arbitrary integer values.

Drunkard’s walk

The so-called drunkard’s walk is a non-trivial Markov chain which starts with value 0 and moves randomly right one step on the number line with probability \(\theta\) and left one step with probability \(1 - \theta\).

The initial value is required to be zero,

\[p_{Y_1}(y_1) \ = \ 1 \ \mbox{ if } \ y_1 = 0.\]Subsequent values are generating with probability \(\theta\) of adding one and probability \(1 - \theta\) of subtracting one,

\[p_{Y_{t+1} \mid Y_t}(y_{t+1} \mid y_t) \ = \ \begin{cases} \theta & \mbox{if } \ y_{t + 1} = y_t + 1, \mbox{and} \[4pt] 1 - \theta & \mbox{if } \ y_{t + 1} = y_t - 1. \end{cases}\]Another way to formulate the drunkard’s walk is by setting \(Y_1 = 0\) and setting subsequent values to

\[Y_{t+1} = Y_t + 2 \times Z_t - 1.\]where \(Z_t \sim \mbox{bernoulli}(\theta).\) Formulated this way, the drunkard’s walk \(Y\) is a transform of the Bernoulli process \(Z\). We can simulate drunkard’s walks for \(\theta = 0.5\) and \(\theta = 0.6\) and see the trend over time.

import numpy as np

M = 10 # Set M to any value you need

theta = 0.5 # Set theta to any value you need

y = np.zeros(M) # Initialize y with zeros

z = np.zeros(M) # Initialize z with zeros

y[0] = 0 # Set the first value of y to 0

# Generate z and y values using the Bernoulli distribution

for m in range(1, M):

z[m] = np.random.binomial(1, theta)

y[m] = y[m - 1] + (1 if z[m] == 1 else -1)

We’ll simulate from both processes for \(M = 1000\) steps and plot.

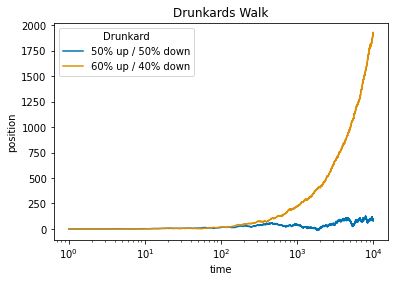

Drunkard’s walks of 10,000 steps with equal chance of going left or right (blue) versus a sixty percent chance of going left (red). The dotted line is drawn at the starting point. As time progresses, the biased random walk drifts further and further from its starting point.

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

np.random.seed(1234)

M = 10000

z1 = np.random.binomial(1, 0.5, M)

z2 = np.random.binomial(1, 0.6, M)

y1 = np.cumsum(2*z1 - 1)

y2 = np.cumsum(2*z2 - 1)

drunkards_df = pd.DataFrame({

'x': np.concatenate([np.arange(1, M+1), np.arange(1, M+1)]),

'y': np.concatenate([y1, y2]),

'drunkard': np.concatenate([np.repeat('50% up / 50% down', M),

np.repeat('60% up / 40% down', M)])

})

drunkards_plot = sns.lineplot(x='x', y='y', hue='drunkard', data=drunkards_df, palette='colorblind')

drunkards_plot.set_xscale('log')

drunkards_plot.set_xlabel('time')

drunkards_plot.set_ylabel('position')

drunkards_plot.set_title('Drunkards Walk')

# Set the legend labels

drunkards_plot.legend(title='Drunkard', labels=['50% up / 50% down', '60% up / 40% down'])

plt.show()

For the balanced drunkard, the expected drift per step is zero as there is equal chance of going in either direction. After 10,000 steps, the expected position of the balanced drunkard remains the origin.^[Contrary to common language usage, the expected position being the origin after \(10,000\) steps does not imply that we should expect the drunkard to be at the origin. It is in fact very unlikely that the drunkard is at the origin after 10,000 steps, as it requires exactly 5,000 upward steps, the probability of which is \(\mbox{binomial}(5,000 \mid 10,000, 0.5) = 0.008.\)] For the unbalanced drunkard, the expected drift per step is \(0.6 \times 1 + 0.4 \times -1 = 0.2\). Thus after 10,000 steps, the drunkard’s expected position is \(0.2 \times 10,000 = 2,000.\)

Gambler’s Ruin

Another classic problem which may be understood in the context of an infinite discrete Markov chain is the gambler’s ruin. Suppose a gambler sits down to bet with a pile of \(N\) chips and is playing a game which costs one chip to play and returns one chip with a probability of \(\theta\).^[The original formulation of the problem, involving two gamblers playing each other with finite stakes, was analyzed in Christiaan Huygens. 1657. Van Rekeningh in Spelen van Geluck. Here we assume one player is the bank with an unlimited stake.] The gambler is not allowed to go into debt, so if the gambler’s fortune ever sinks to zero, it remains that way in perpetuity. The results of the bets at times \(t = 1, 2, \ldots\) can be modeled as an independent and identically distributed random process \(Z = Z_1, Z_2, \ldots\) with

\[Z_t \sim \mbox{bernoulli}(\theta).\]As usual, a successful bet is represented by \(Z_t = 1\) and an unsuccessful one by \(Z_t = 0\). The gambler’s fortune can now be defined recursively as a time series \(Y = Y_1, Y_2, \ldots\) in which the initial value is given by

\[Y_1 = N\]with subsequent values defined recursively by

\[Y_{n + 1} \ = \ \begin{cases} 0 & \mbox{if} \ Y_n = 0, \ \mbox{and} \[4pt] Y_n + Z_n & \mbox{if} \ Y_n > 0. \end{cases}\]Broken down into the language of Markov chains, we have an initial distribution concentrating all of its mass at the single point \(N\), with mass function

\[p_{Y_1}(N) = 1.\]Each subsequent variable’s probability mass function is given by

\[p_{Y_{t + 1} \mid Y_t}(y_{t + 1} \mid y_t) \ = \ \begin{cases} \theta & \mbox{if} \ y_{t + 1} = y_t + 1 \[4pt] 1 - \theta & \mbox{if} \ y_{t + 1} = y_t - 1. \end{cases}\]These mass functions are all identical in that \(p_{Y_{t+n+1} \mid Y_{t + n}} = p_{Y_{t + 1} \mid Y_t}.\) In other words, \(Y\) is a time-homogeneous Markov chain.

We are interested in two questions pertaining to the gambler. First, what is their expected fortune at each time \(t\)? Second, what is the probability that they have fortune zero at time \(t\).^[A gambler whose fortune goes to zero is said to be ruined.] Both of these calculations have simple simulation-based estimates.

Let’s start with expected fortune and look out \(T = 100\) steps. Suppose the chance of success on any given bet is \(\theta\) and their initial fortune is \(N\). The simulation of the gambler’s fortune is just a straightforward coding of the time series.

import numpy as np

# Set initial values

N = 10

T = 100

theta = 0.5

y = np.zeros(T)

z = np.zeros(T)

# Set initial value of y

y[0] = N

# Simulate the process

for t in range(1, T):

z[t] = np.random.binomial(1, theta)

y[t] = y[t - 1] + (1 if z[t] else -1)

print(y)

[10. 11. 10. 9. 10. 9. 10. 9. 10. 11. 12. 13. 12. 13. 14. 13. 14. 15.

14. 13. 14. 15. 14. 13. 12. 11. 10. 11. 12. 11. 12. 13. 12. 11. 12. 11.

10. 9. 8. 9. 8. 7. 8. 9. 10. 11. 12. 11. 10. 11. 10. 9. 8. 7.

6. 5. 4. 3. 2. 3. 4. 3. 2. 3. 2. 3. 2. 3. 4. 3. 4. 3.

2. 3. 4. 5. 4. 3. 2. 1. 2. 3. 4. 5. 4. 3. 2. 3. 4. 5.

6. 5. 6. 7. 6. 5. 4. 5. 6. 7.]

Now if we simulate that entire process \(M\) times, we can calculate the expected fortune as an average at each time \(t \in 1:T\).

import numpy as np

# Set initial values

N = 10

T = 100

M = 1000

theta = 0.5

y = np.zeros((M, T))

z = np.zeros((M, T))

expected_fortune = np.zeros(T)

# Simulate the process for each m in M

for m in range(M):

y[m][0] = N

for t in range(1, T):

z[m][t] = np.random.binomial(1, theta)

y[m][t] = y[m][t - 1] + (1 if z[m][t] else -1)

# Calculate expected fortune at each time point

for t in range(T):

expected_fortune[t] = np.mean(y[:, t])

print(expected_fortune)

[10. 9.976 9.982 9.986 9.97 9.954 9.992 10.006 9.97 9.986

9.966 9.984 9.924 9.912 9.838 9.836 9.81 9.78 9.822 9.878

9.868 9.826 9.86 9.848 9.868 9.876 9.824 9.824 9.78 9.776

9.788 9.824 9.86 9.93 9.896 9.878 9.864 9.886 9.896 9.938

9.984 9.962 9.932 9.982 9.996 9.978 9.968 9.948 9.952 9.996

10.032 10.036 10.02 9.976 10.004 9.998 9.988 9.982 9.996 10.046

10.004 9.978 9.946 9.994 9.974 9.94 9.898 9.838 9.828 9.808

9.818 9.85 9.852 9.826 9.816 9.81 9.734 9.712 9.732 9.73

9.726 9.776 9.74 9.748 9.772 9.778 9.772 9.74 9.754 9.7

9.72 9.73 9.674 9.71 9.696 9.7 9.764 9.788 9.806 9.858]

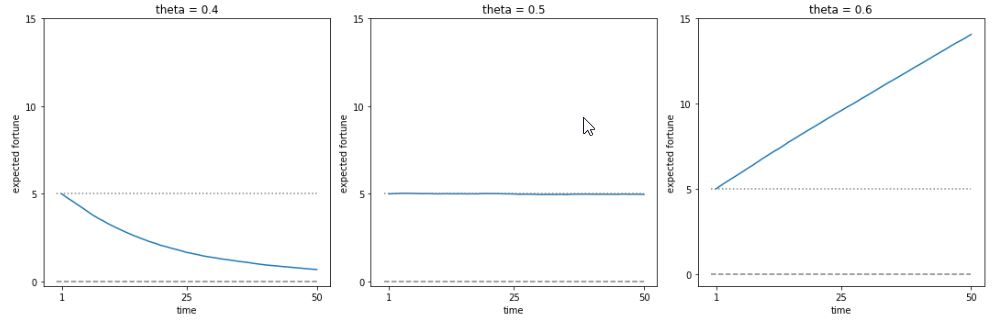

Let’s run \(M = 10,000\) simulations for \(T = 50\) starting with a stake of \(N = 5\) with several values of \(\theta\) and plot the expected fortunes.

Expected returns for gambler starting with stake \(N\) and having a \(\theta\) chance at each time point of increasing their fortune by 1 and a \(1 - \theta\) chance of reducing their fortune by 1. The horizontal dotted line is at the initial fortune and the dashed line is at zero.

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy.stats import bernoulli

from functools import partial

from itertools import product

from tqdm import tqdm

# Define functions

def simulate_fortune(theta, N=5, T=50):

y = np.empty((T+1,))

y[0] = N

for t in range(1, T+1):

if y[t-1] == 0:

y[t] = 0

else:

y[t] = y[t-1] + np.random.choice([-1, 1], p=[1-theta, theta])

return y

def expected_fortune(theta, M=10000, N=5, T=50):

y = np.empty((M, T+1))

for m in range(M):

y[m] = simulate_fortune(theta, N=N, T=T)

return np.mean(y[:, 1:], axis=0)

# Set parameters

np.random.seed(1234)

N = 5

T = 50

M = 10000

Theta = [0.4, 0.5, 0.6]

# Simulate and plot expected fortune

df_ruin = pd.DataFrame(columns=['time', 'expected_fortune', 'theta'])

for theta in Theta:

expected_fortune_theta = expected_fortune(theta, M=M, N=N, T=T)

df_theta = pd.DataFrame({'time': range(1, T+1),

'expected_fortune': expected_fortune_theta,

'theta': ['theta = {}'.format(theta)]*T})

df_ruin = pd.concat([df_ruin, df_theta])

# Plot

fig, axes = plt.subplots(nrows=1, ncols=3, figsize=(15, 5))

for i, theta in enumerate(Theta):

df_theta = df_ruin[df_ruin['theta'] == 'theta = {}'.format(theta)]

ax = axes[i]

ax.plot(df_theta['time'], df_theta['expected_fortune'])

ax.axhline(y=N, linestyle=':', color='gray', linewidth=0.5)

ax.axhline(y=0, linestyle='--', color='gray', linewidth=0.5)

ax.set_title('theta = {}'.format(theta))

ax.set_xlabel('time')

ax.set_ylabel('expected fortune')

ax.set_xticks([1, 25, 50])

ax.set_yticks([0, 5, 10, 15])

plt.tight_layout()

plt.show()

Next, we’ll tackle the problem of estimating the probability that a gambler has run out of money at time \(t\). In symbols, we are going to use simulations \(y^{(1)}, \ldots, y^{(M)}\) of the gambler’s time series,

Expected Fortune over Time for Different Values of \(\Theta\)

This last term can be directly calculated by adding the indicator variables to the calculations before.

for m in range(M):

y[m, 0] = N

for t in range(1, T):

z = np.random.binomial(1, theta)

y[m, t] = y[m, t - 1] + (1 if z else -1)

ruined[m, t] = (y[m, t] == 0)

for t in range(T):

estimated_pr_ruin[t] = np.mean(ruined[:, t])

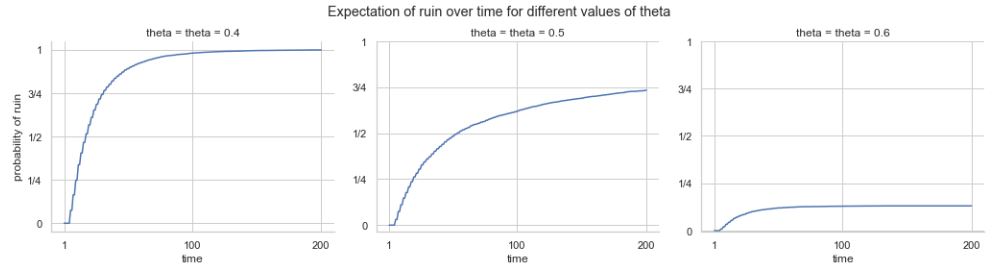

So let’s run that and plot the probability of ruin for the same three choices of \(\theta\), using \(M = 5,000\) simulations. But this time, we’ll run for \(T = 200\) time steps.

Probability of running out of money for a gambler starting with stake \(N\) and having a \(\theta\) chance at each time point of increasing their fortune by 1 and a \(1 - \theta\) chance of reducing their fortune by 1. The horizontal dotted line is at 100 percent.

import numpy as np

import pandas as pd

import seaborn as sns

import matplotlib.pyplot as plt

np.random.seed(1234)

N = 5

T = 200

M = 5000

Theta = [0.4, 0.5, 0.6]

df_expect_ruin = pd.DataFrame(columns=['x', 'y', 'theta'])

for theta in Theta:

y = np.empty((M, T))

for m in range(M):

y[m, 0] = N

for t in range(1, T):

if y[m, t - 1] == 0:

y[m, t] = 0

else:

z = np.random.binomial(1, theta)

y[m, t] = y[m, t - 1] + (1 if z else -1)

pr_ruin = np.mean(y == 0, axis=0)

df_theta = pd.DataFrame({

'x': range(1, T+1),

'y': pr_ruin,

'theta': [f'theta = {theta}'] * T

})

df_expect_ruin = pd.concat([df_expect_ruin, df_theta], ignore_index=True)

sns.set_theme(style="whitegrid")

g = sns.relplot(

data=df_expect_ruin, x='x', y='y',

col='theta', kind='line', facet_kws=dict(sharey=False),

col_wrap=3, height=4, aspect=1.2

)

g.set_axis_labels('time', 'probability of ruin')

g.set(xticks=[1, 100, 200], yticks=[0, 0.25, 0.5, 0.75, 1],

yticklabels=['0', '1/4', '1/2', '3/4', '1'])

g.fig.subplots_adjust(top=0.85)

g.fig.suptitle('Expectation of ruin over time for different values of theta')

plt.show()

Even in a fair game, after 50 bets, there’s nearly a 50% chance that a gambler starting with a stake of 5 is ruined; this probabiltiy goes up to nearly 75% after 200 bets.

Queueing

Suppose we have a checkout line at a store (that is open 24 hours a day, 7 days a week) and a single clerk. The store has a queue, where customers line up for service. The queue begins empty. Each hour a random number of customers arrive and a random number of customers are served. Unserved customers remain in the queue until they are served.

To make this concrete, suppose we let \(U_t \in 0, 1, \ldots\) be the number of customers that arrive during hour \(t\) and that it has a binomial distribution,

\[U_t \sim \mbox{binomial}(1000, 0.005).\]Just to provide some idea of what this looks like, here are 20 simulated values,

import numpy as np

M = 20

y = np.random.binomial(n=1000, p=0.005, size=M)

for m in range(M):

print(f"{y[m]:2.0f}", end=" ")

6 7 6 9 8 8 5 5 7 2 2 4 5 7 5 0 3 2 6 4

We can think of this as 1000 potential customers, each of which has a half percent chance of deciding to go to the store any hour. If we repeat, the mean number of arrivals is 5 and the standard deviation is 2.2.

Let’s suppose that a clerk can serve up to \(V_t\) customers per hour, determined by the clerk’s rate \(\phi\),

\[V_t \sim \mbox{binomial}(1000, \phi).\]If \(\phi < 0.005,\) there is likely to be trouble. The clerk won’t be able to keep up on average.

The simulation code just follows the definitions.

import numpy as np

queue = np.zeros(T) # Initialize queue array to zeros

queue[0] = 0 # Set first element to 0

for t in range(1, T):

arrive[t] = np.random.binomial(n=1000, p=0.005)

serve[t] = np.random.binomial(n=1000, p=phi)

queue[t] = max(0, queue[t-1] + arrive[t] - serve[t])

The max(0, ...) is to make sure the queue never gets negative. If

the number served is greater than the total number of arrivals and

customers in the queue, the queue starts empty the next time step.

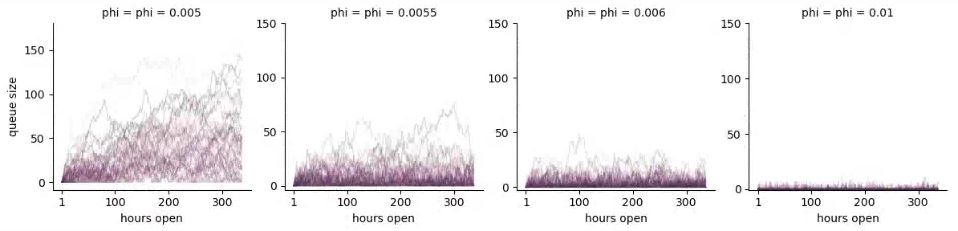

Let’s try different values of \(\phi\), the average server rate, and plot two weeks of service.^[\(24 \mbox{hours/day} \ \times 14 \ \mbox{days} = 336 \mbox{hours}\)]

Multiple simulations of queue size versus time for a queue with \(\mbox{binomial}(1000, 0.005)\) customers arriving per hour (an average of 5), and a maximum of \(\mbox{binomial}(1000, \phi)\) customers served per hour, plotted for various \(\phi\) (as indicated in the row labels).

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

np.random.seed(1234)

T = 14 * 24

run = 1

queue = np.empty(T)

queue[:] = np.nan

queue_df = pd.DataFrame({'t': [], 'queue': [], 'run': [], 'phi': []})

for m in range(50):

for phi in [0.005, 0.0055, 0.006, 0.01]:

queue[0] = 0

for t in range(1, T):

arrived = np.random.binomial(n=1000, p=0.005, size=1)

served = np.random.binomial(n=1000, p=phi, size=1)

queue[t] = max(0, queue[t-1] + arrived - served)

df = pd.DataFrame({

't': range(1, T+1),

'queue': queue,

'run': np.repeat(run, T),

'phi': np.repeat(f'phi = {phi}', T)

})

queue_df = pd.concat([queue_df, df])

run += 1

grid = sns.FacetGrid(queue_df, col='phi', sharey=False)

grid.map(sns.lineplot, 't', 'queue', 'run', alpha=0.2, linewidth=0.9,color='blue')

grid.set(xticks=[1, 100, 200, 300], yticks=[0, 50, 100, 150])

grid.set_axis_labels(x_var='hours open', y_var='queue size')

plt.show()

As can be seen in the plot, the queue not growing out of control is very sensitive to the average service rate per hour. At an average rate of five customers served per hour (matching the average customer intake), the queue quickly grows out of control. With as few as five and a half customers served per hour, on average, it becomes stable long term; with seven customers served per hour, things settle down considerably. When the queue goes up to 50 people, as it does with \(\phi = 0.0055\), wait times are over ten hours. Because of the cumulative nature of queues, a high server capacity is required to deal with spikes in customer arrival.

Key Points